What volumes of fossil oil and other fuels are consumed in maritime shipping? What is the volume trend and what progress is being made in terms of decarbonization?

1. Total volumes in 2025 and 2026

Fuel consumption in international shipping has been rising significantly since 2023. Bunker sales (marine fuel sales at seaports) have returned to pre-Covid levels.

🔴 In 2025, consumption by international maritime shipping (vessels >5,000 GT) increased by 2.0% from 245.1 million tonnes (IMO) to approx. 250 million tonnes. Bunker sales data from a large sample of major seaports , which cover 60% of total demand demonstrate this.

This data does not capture the fuel consumption of LNG carriers, which obtain their fuel through the boil-off gas from their cargo or at the LNG export terminal. However, this market segment also grew at comparable rates in 2024 and 2025.

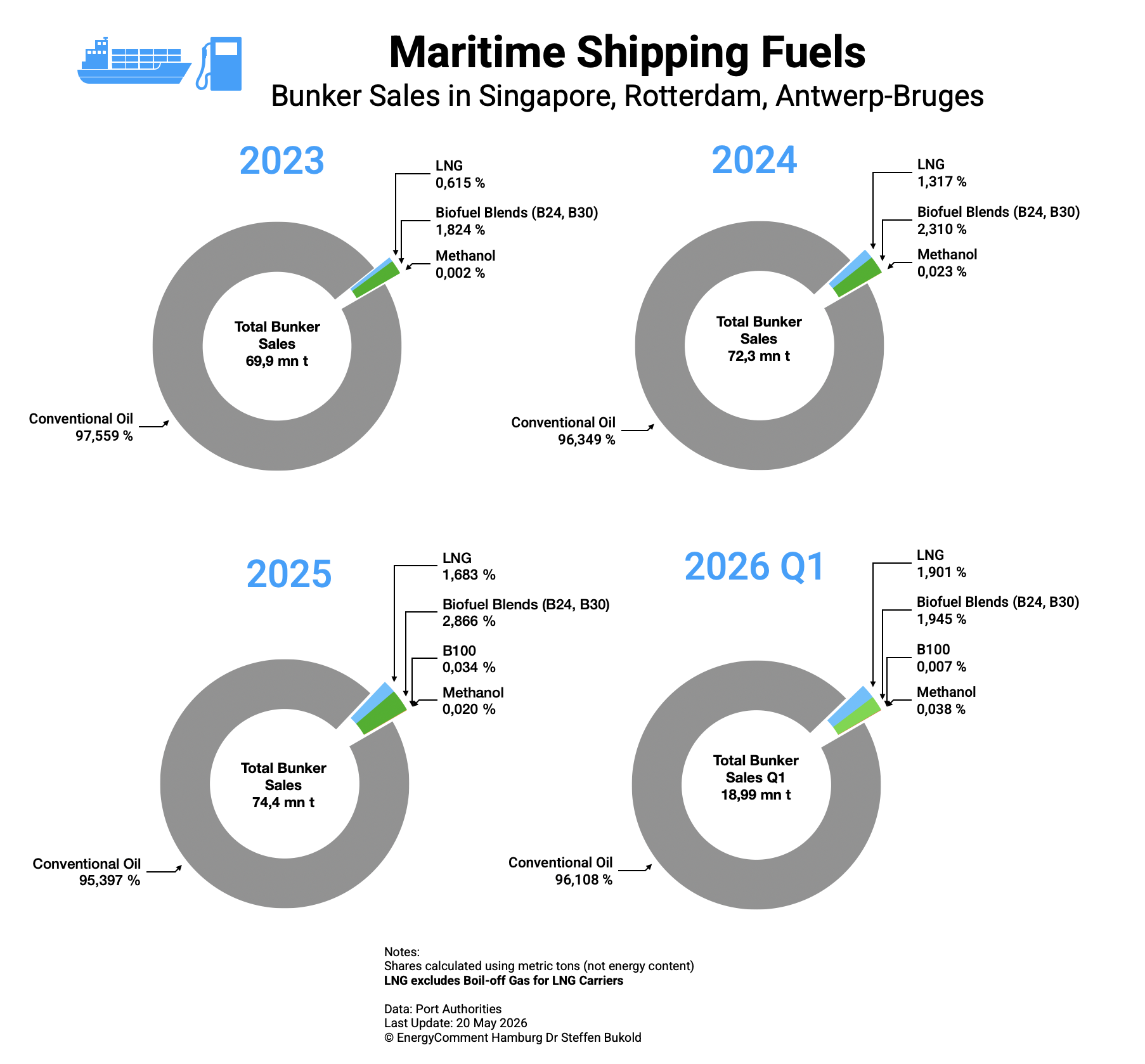

2. The fuel mix 2023-2026

2.1 Bunker ports – our sample

Major ports provide timely and detailed data on the structure of fuel consumption. The chart shows bunker sales (i.e. sales of marine fuels) in Singapore, Rotterdam, and Antwerp-Bruges. This sample captures approximately 30% of global bunker volumes.

Singapore is by far the world’s most important bunker port. Nearly 23% of global bunker sales were handled there last year (56.8 million tonnes). Rotterdam ranked second with 9.2 million tonnes. Antwerp-Bruges ranked not far behind (7.9 million tonnes). Our sample thus captures No. 1, No. 2, and No. 5 of global ports.

2.2 Fuel Mix 2023-2026

🔹 Oil

🔴 The chart shows that the share of fossil oil fuels (fuel oil; gasoil/diesel) has declined only slightly in recent years: from 97.6% in 2023 to 95.4% in 2025 and 96.1% in the first quarter of 2026.

Note:

The charts show distribution by tonnes. In energy terms, the share of low-carbon fuels is even somewhat lower. While fossil oil (HFO/VLSFO) provides approximately 40-41 GJ/t, biodiesel/UCOME provides only 37-38 GJ/t and methanol only 20 GJ/t (ammonia 18.6 GJ/t; LNG 48-50 GJ/t).

🔹 LNG

The share of fossil natural gas (LNG) rose from 0.6% (2023) to 1.7% (2025) and 1.9% of bunker sales (Q1/2026).

While LNG produces approximately 20% less CO₂ than fuel oil for the same propulsion energy in the ship engine, there are methane emissions in the supply chain (WTW) and in the engine. The energy expenditure for liquefying natural gas to LNG is also very high (approximately 8% of feed gas).

On balance, the climate benefit of LNG compared to fuel oil is at best small, and in some cases near zero or even negative.

It is important to note that LNG already plays a considerably larger role as marine fuel than bunker sales data suggest. In 2025 the LNG bunker market (excluding LNG carriers) reached approx. 3.8 million tons of LNG, according to Lansdowne Moritz estimates.

However, in addition to that, about 15-17 million tons of LNG were consumed by LNG carriers as boil-off gas during transit and via bunkering at LNG export terminals. These volumes do not appear in port bunkering statistics.

🔹 Bioblends and B100

Biofuel blending (primarily UCO-FAME) with a bio-share of 24% (B24) or 30% (B30) enables partial decarbonization, especially when using waste fuels.

Bioblends provided 2.9% of marine fuels in our sample in 2025 and just 1.9% in the first quarter of 2026. The share of biofuels (100%) was therefore slightly below 1% in 2025.

Since 2025, Singapore has also recorded bunker sales of pure biofuels (B100), though these remain very small at 0.03% of total fuel volumes in 2025 and even less in Q1/2026.

🔹 New Fuels: Methanol, Ammonia, Bio-LNG

Methanol volumes also remain very low so far at just 0.02% in 2024 and 2025. In the first quarter of 2026 the share doubled to roughly 0.04%. Bio-LNG (liquefied biomethane) and ammonia volumes are currently in a negligible range or are still in the testing phase.

While shipping lines are reporting some ammonia or methanol volumes, this almost always involves mass balance calculations, meaning the low-carbon fuels are deployed elsewhere while the climate benefits are allocated to the vessel.

3. Decarbonization of shipping fuels – the bottom line

On balance, actual decarbonization of shipping fuels has been very limited so far and stands in clear contrast to the large number of dual-fuel vessels in operation or in the orderbook that could use methanol or ammonia.

🔴 🔴 From the 4.5% „alternative fuels“ deployed in our port sample in 2025, actual decarbonization amounts to about 0.9-1.1% of bunker sales (excluding LNG Carriers), accounting for different energy contents and the CO₂ footprint of biofuels. Given the limited progress made in the years 2023 to 2026, „net-zero shipping“ by 2050 is obviously out of reach.

All major shipping lines in the top 10 have the corporate goal of operating net-zero by 2050. It remains completely unclear in what mix and from what sources low-carbon fuels can be provided for this purpose.

Ship orderbooks and now also port infrastructure show considerable advance investments. But without price alignment and better availability of low-carbon fuels, the transition to net-zero maritime shipping will not succeed.

Your comment

- Please use our contact form

- Picture: AI (Open AI)