Quick Summary

- Numbers point toward full-year 2025 sales of approximately 21 million EVs, slightly below expectations.

- This would represent a global 24% car market share and a 20% year-on-year growth in unit volumes.

- Regional trajectories diverge: our projections indicate contraction in the United States (-3%), modest growth in China (+15%), substantial expansion in the European Union (+25%), and robust acceleration in other global regions (+40%).

Main Findings

Global EV Adoption: Only Modest Pace in 2025

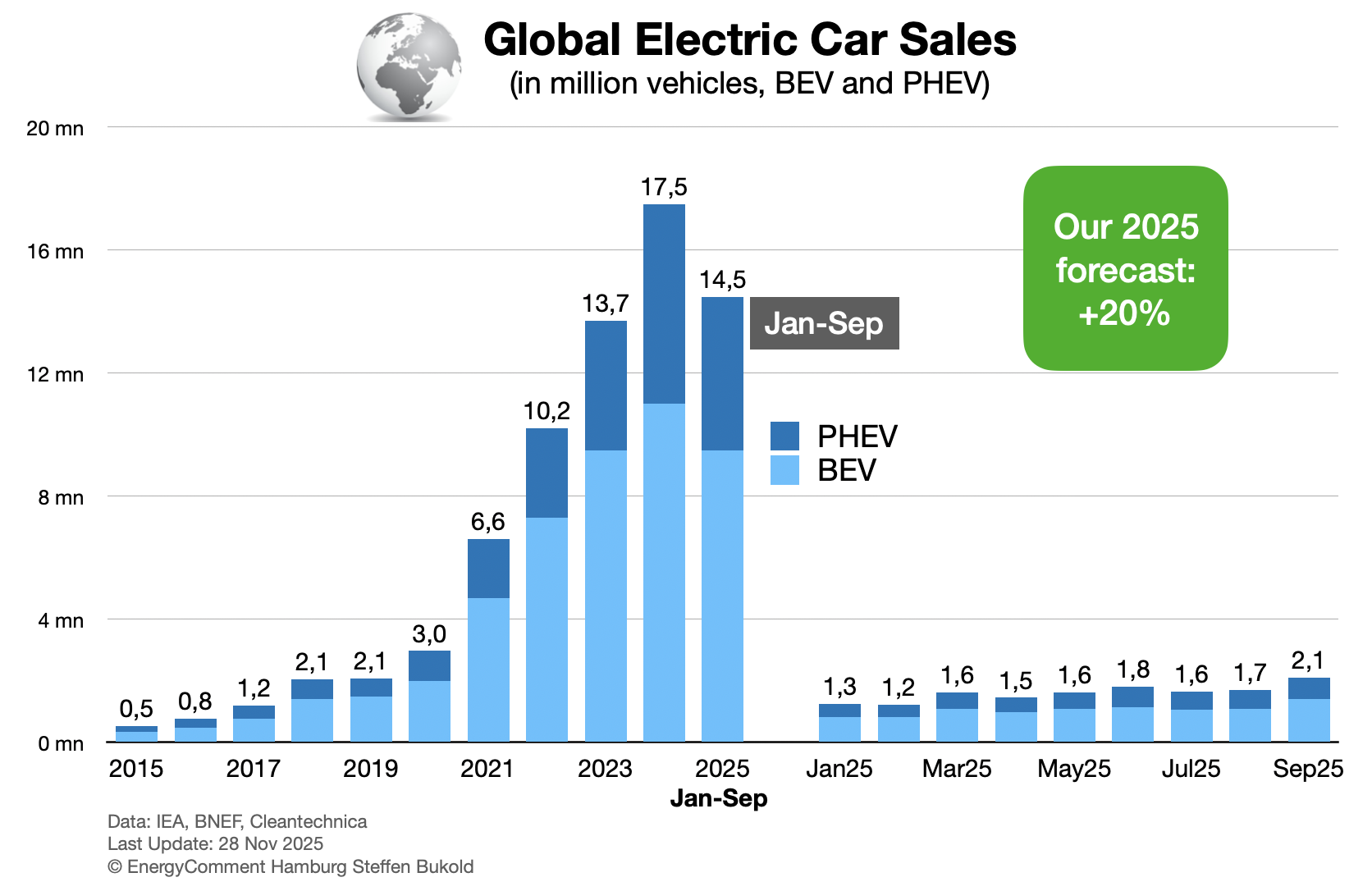

The electrification of the global automotive fleet continues to progress slowly this year. Data show sales of 14.5 million EVs in the first nine months, with October figures expected to match September levels.

The numbers thus point toward full-year 2025 sales of approximately 21 million EVs. This would represent a 24% market share and a 20% year-on-year growth in unit volumes in our forecast (see chart)

BNEF analysts project slightly higher figures, forecasting 21.9 million EVs and a 25% global market share. Rho Motion, meanwhile, estimates the EV market share at 23% for the January-October 2025 period.

Last year’s market share stood at 22%. An advance from 22% to 23-25% in 2025 would therefore prove disappointing.

Headwinds come from two markets: the United States and China.

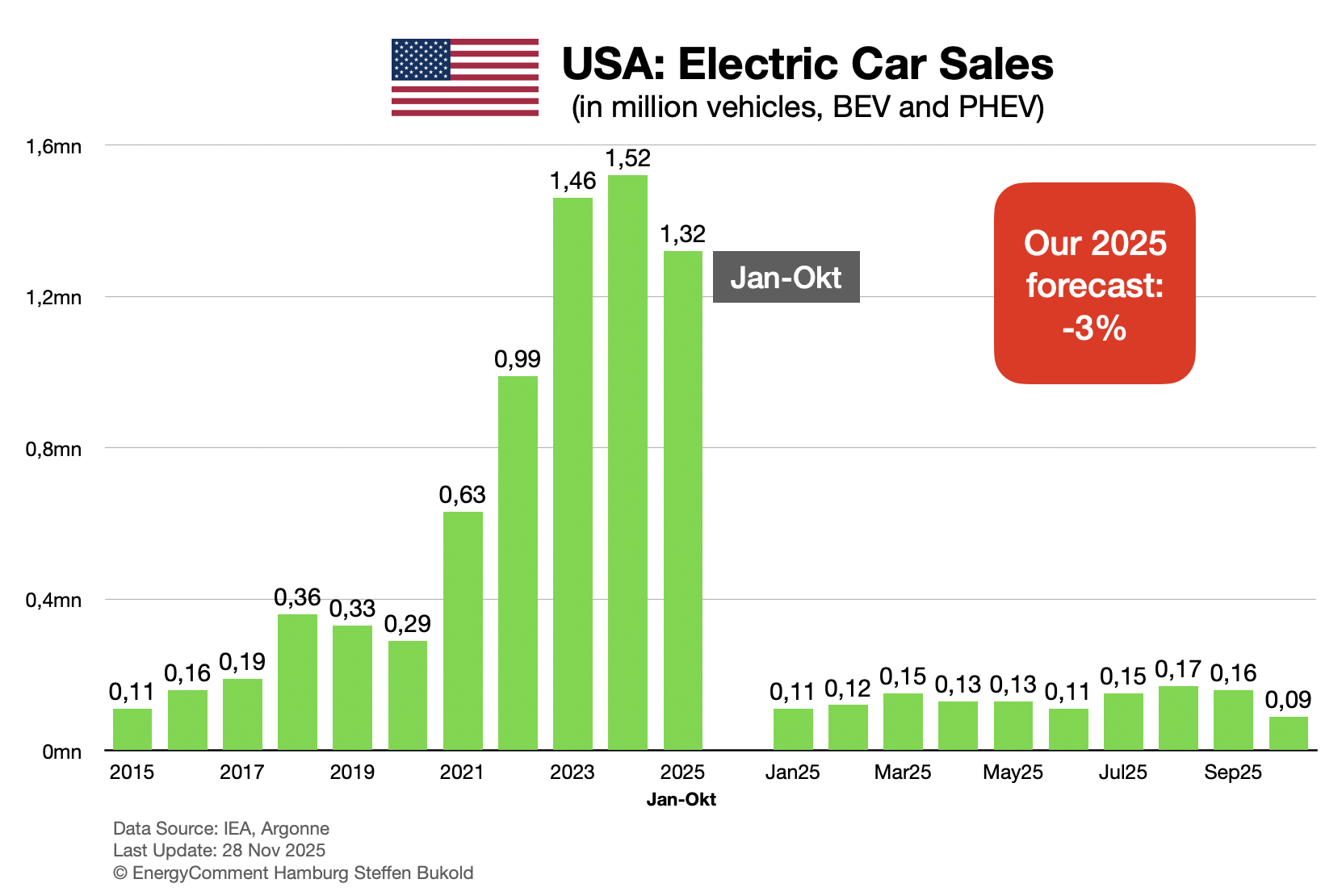

United States

Weakness in US sales has been anticipated since President Trump’s inauguration in January. Federal incentives that supported the market for 15 years—including tax credits and leasing credits—expired at the end of September.

This triggered a September spike followed by an October collapse. November and December figures are likewise expected to disappoint. S&P Global projects market share falling to just 7%. Only state-level support in California, the nation’s largest automotive market, along with manufacturer discounting, prevents an even steeper decline.

The US transportation transition has effectively stalled, as the internal combustion engine fleet expands by a net 4 million vehicles annually, substantially outpacing the 1.5 million new EV registrations.

Our forecast indicates a 3% decline in new EV registrations this year (see chart).

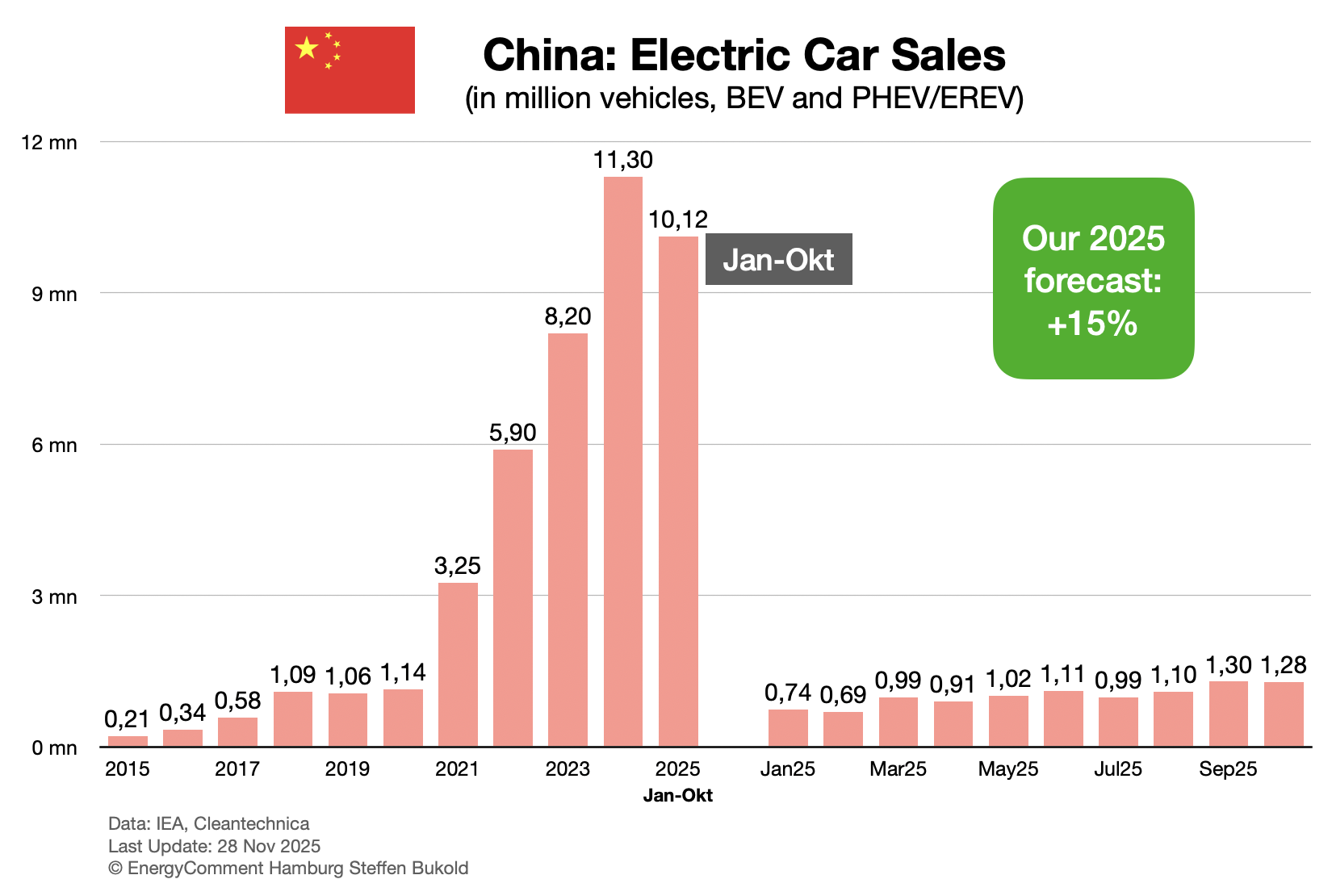

China

China is also experiencing the expiration of several EV incentives, including purchase tax breaks and trade-in payments. October figures already showed a modest decline compared to September.

On a positive note, the market is shifting toward higher penetration of pure battery electric vehicles (BEV), while plug-in hybrid registrations (PHEV) contract. Overall EV share of new vehicle sales has already exceeded 50% for several months. BEVs alone command approximately a market share of one third this year.

Saturation levels have been reached in several metropolitan areas. Nevertheless, continued market growth appears assured. Our forecast calls for 15% growth in new registrations for 2025.

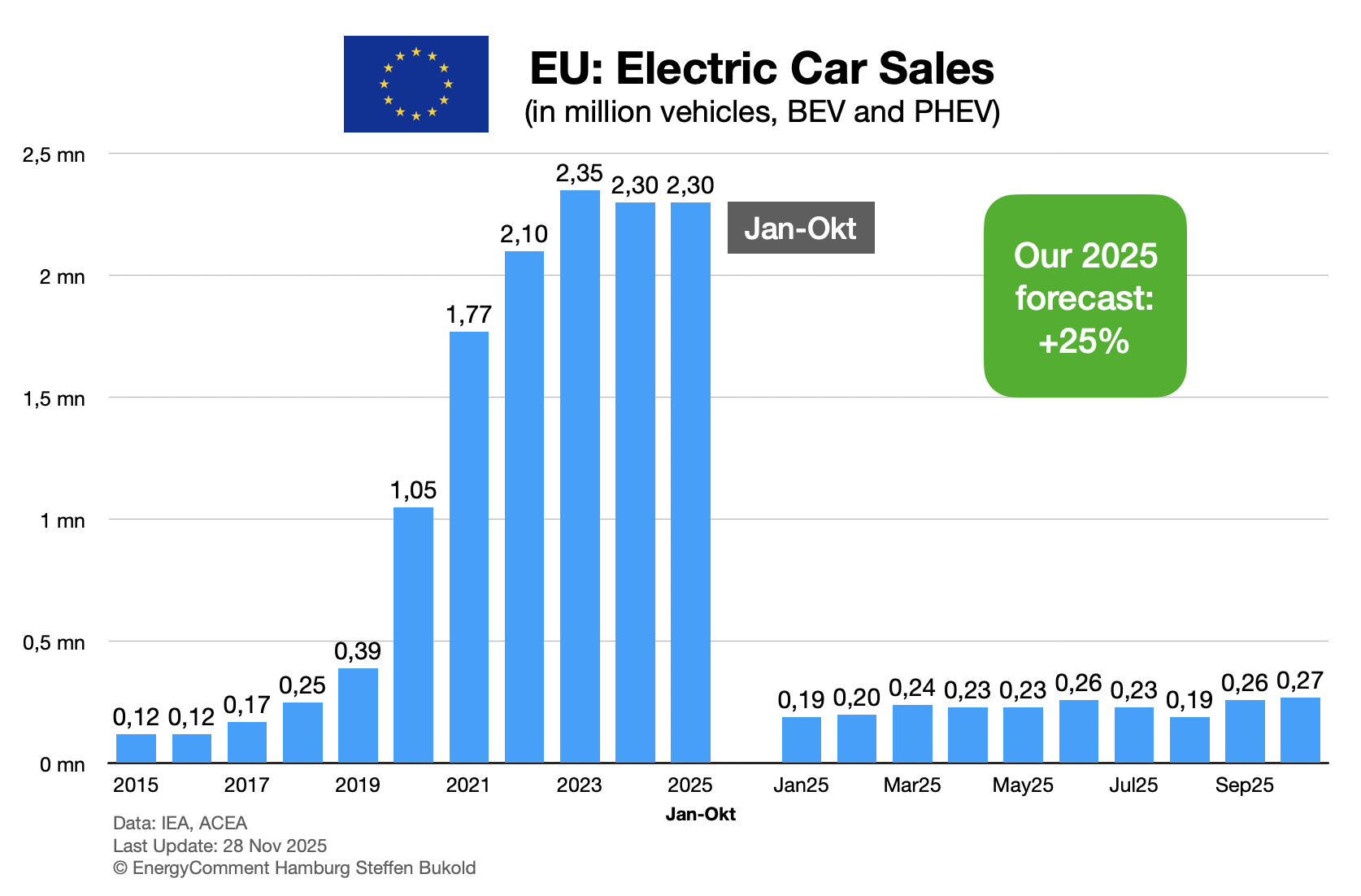

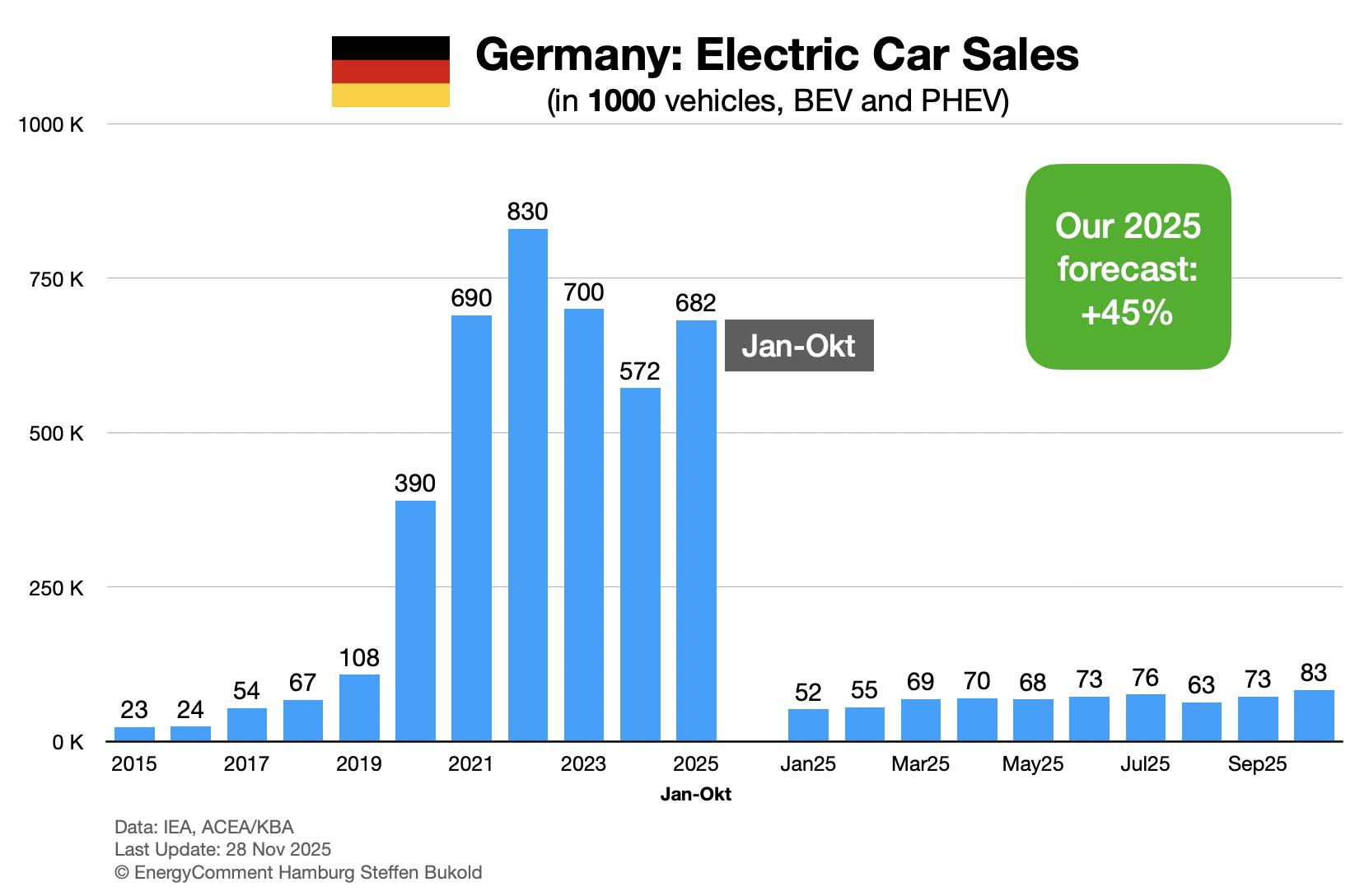

EU and Germany

The European Union is recovering from last year’s setback. October figures already surpassed full-year 2024 totals. Our projection indicates a 25% growth in EV registrations for 2025.

Germany shows particularly robust momentum. We anticipate a growth rate of 45% this year. Even so, EV volumes will remain below the 2022 peak.

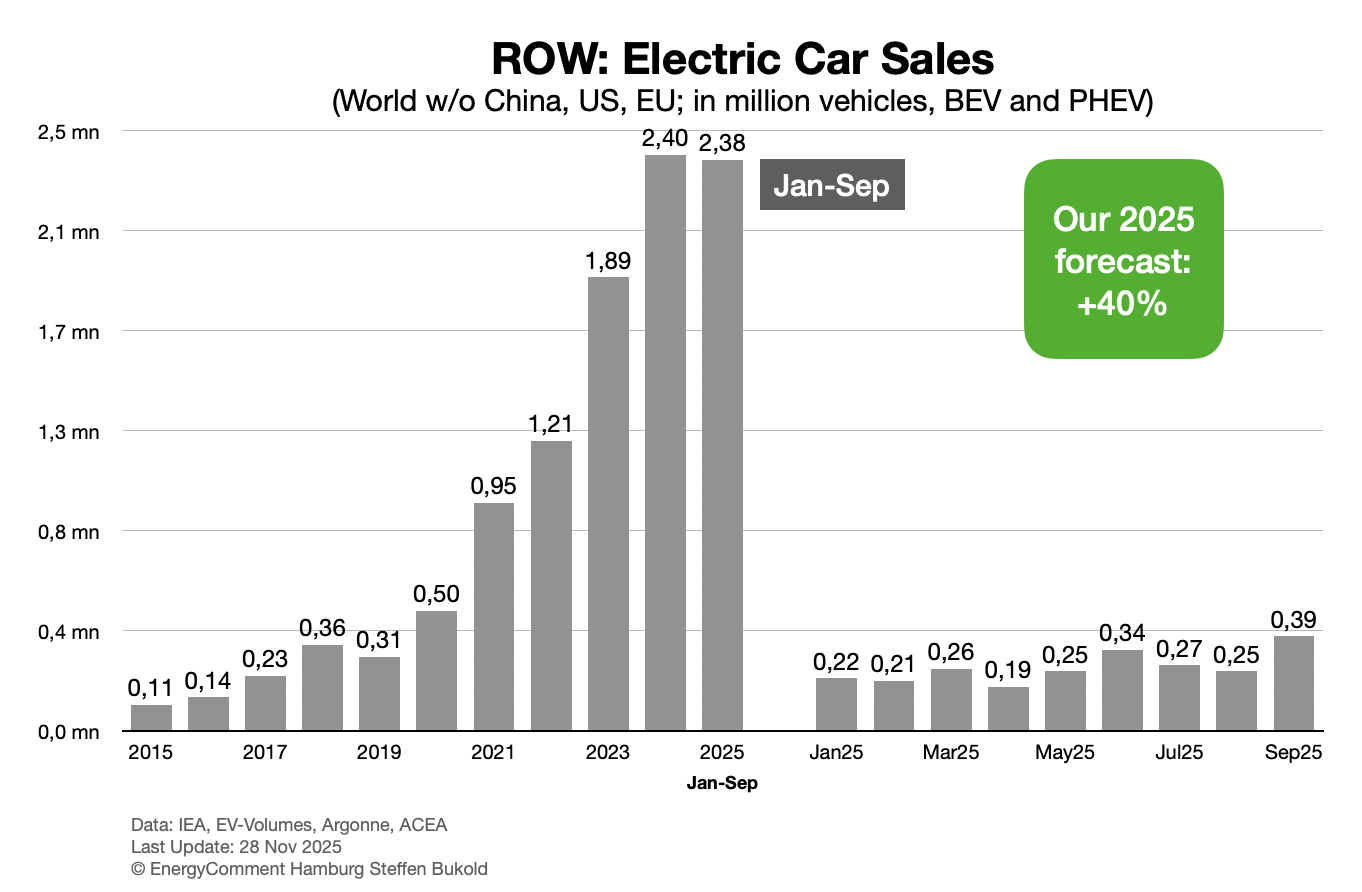

Rest of World

RoW, i.e. markets outside China, the EU, and US demonstrate highly positive trajectories. Wherever Chinese export initiatives face no import barriers, adoption rates surge dramatically.

This applies particularly to the UK which reached a 38% EV market share in October, along with numerous Latin American, South and Southeast Asian nations.

By September, the RoW volumes had already matched full-year 2024 totals. Forecasts therefore call for a substantial 40% growth in EV registrations.

Your comment

- Please use our contact form

Comments

One response to “Global EV Adoption: Modest Pace in 2025 (Update November 2025)”

[…] Headlines in 2025 still focus on electric vehicles, but the vehicle parc on the road tells a different story. EV sales are growing, yet recent analysis shows global EV volumes in 2025 are slightly below earlier expectations, with regional growth patterns diverging. energycomment.de […]