1. New ship orders in November 2025

New ship orders in November reflect waning interest in low-carbon propulsion systems, as DNV reports.

DNV reported merely 10 orders for non-conventional propulsion that does not rely exclusively on fossil oil products as fuel, namely fuel oil or gasoil. All 10 vessel orders will utilize LNG.

🔴 Since virtually only fossil natural gas is employed in practice, November saw not a single order for low-carbon options such as methanol, ammonia, or hydrogen.

2. New ship orders January – November 2025

The balance sheet for the year’s first 11 months now records 232 non-conventional orders. Of these, 157 are for LNG (excluding LNG carriers) and 19 for LPG (propane, butane)—both fossil energy carriers.

🔴 Methanol accounts for 47 orders this year to date, ammonia for 5, and hydrogen for 4 orders. These potential low-carbon propulsion systems, however, predominantly comprise dual-fuel drives that can also utilize fossil fuel oil.

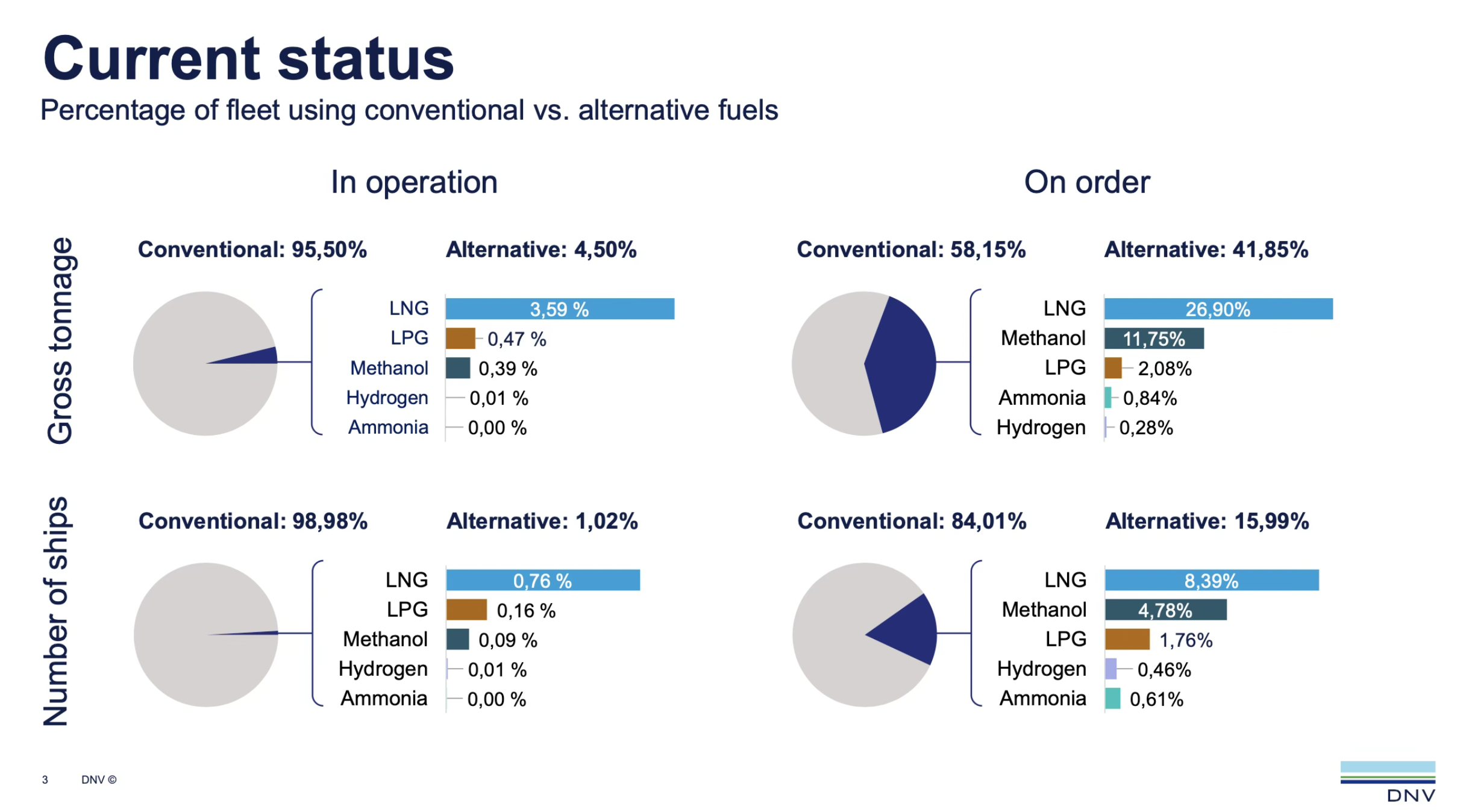

3. The Global Fleet: Current Status

The existing fleet remains dominated by vessels using exclusively fossil oil products (fuel oil, gasoil) as fuel.

🔴 As of November 2025, this applies to 95.5% of gross tonnage and nearly 99% of vessels, DNV reports. Excluding the likewise fossil fuels LNG and LPG, currently only 0.4% of the fleet (gross tonnage) or 0.1% of the fleet (vessel count) can deploy low-carbon fuels. These consist almost exclusively of methanol.

Battery/hybrid propulsion systems also play no major role, representing 0.4% (gross tonnage) and 0.8% (vessel count) respectively (data here as of August 2025).

The complete order book shows a different, markedly broader distribution of propulsion types.

🔴 58% of ordered gross tonnage will use exclusively fossil oil. A further 27% will employ LNG and 2% LPG. Methanol currently accounts for nearly 12%, ammonia for 0.8%, and hydrogen for 0.3% of ordered vessels. Since these comprise almost exclusively dual-fuel propulsion systems, deployment of low-carbon fuels is not assured.

Examining vessel counts, the order book shows an 84% share for fossil oil, plus 8% for LNG and 2% for LPG. Only 6% of ordered vessels utilize low-carbon fuels, nearly all methanol (5%), while hydrogen (0.5%) and ammonia (0.6%) remain marginal.

Source: DNV

Understanding „Capable“ vs. „Ready“

Vessels designated „methanol-capable“ or „ammonia-capable“ are often conflated with those merely „methanol-ready“ or „ammonia-ready“.

„Capable“ signifies vessels can deploy the fuel without further modifications. The „ready“ status is vaguely and inconsistently defined. It requires additional investment and a shipyard visit before the fuel can actually be utilized.

Your comment

- Please use our contact form

- Picture: BFL-Flux

Comments

2 Kommentare zu „Maritime Shipping: Orderbook and Low-Carbon Fuels (November 2025)“

[…] of shipping fuels has been very limited so far and stands in clear contrast to the large number of dual-fuel vessels in operation or in the orderbook that could use methanol or […]

[…] of shipping fuels has been very limited so far and stands in clear contrast to the large number of dual-fuel vessels in operation or in the orderbook that could use methanol or […]